Digital transformation in the insurance industry is in full swing, yet the organization and management of processes at most traditional insurers have barely changed in recent years. In fact, digital disruption has already hit insurers with full force and a lasting impact on profitability. What are the consequences, and what can we do about it?

On the one hand, the current pandemic is acting as a catalyst for companies, and on the other hand—depending on the customer base—it’s providing a respite in which executives and managers can reconsider the consequences of individual, departmental, and divisional decisions within the overall context of the organization (COR). However, the challenges for insurance companies remain: implementing changes in response to current trends and user behavior more quickly and dynamically.

“Low code” can be key to rapid response times and offers insurers and brokers new, profitable opportunities. The combination of pre-programmed, sophisticated code with a graphical user interface allows subject matter experts to customize IT applications without requiring in-depth programming knowledge.

But what exactly is low code?

Low-code could be described as a booster for digitalization: When Apollo 11 lifted off from the Kennedy Space Center on July 16, 1969, the astronauts’ lives depended almost entirely on the quality of the control software developed by Margaret Hamilton. She and her team had developed, tested, verified, and installed the software entirely in machine language (assembler) on the rocket. The development involved an estimated total effort of 1,400 full-time years. The source code was only about 3 MB in size!

Since the launch of Apollo 11, much has changed: Today, no one programs basic functions “by hand” anymore. Libraries, frameworks, cloud services, and APIs are systematically used and reused – the amount of handwritten source code is rapidly decreasing. Low-code goes a step further, combining templates or pre-programmed functions with a simple and intuitive graphical user interface. With these features, low-code platforms facilitate the development of complex applications with minimal programming effort.

The partial automation of many manual tasks leads to a significant speed advantage in the development of new solutions. The associated short implementation cycles enable rapid validation and iterative improvement. Low-code platforms allow for the partial automatic creation of data structures, visual modeling of processes, and the execution of time-consuming tests. At the same time, department employees can also take on tasks that previously required in-depth programming knowledge.

And what does that mean for the insurance industry?

Low-code technology helps to create and execute IT applications more quickly at various points along the insurance value chain. This is achieved immediately, always operating invisibly in the background and ideally maintained by experienced digitalization experts. This opens up interesting opportunities for the insurance industry and can contribute to solving pressing problems.

In agile project management, the term “fail-fast” is often used, which refers to the ability to identify errors early on. However, to prevent a new idea from failing before it has even been tested in the market, suitable and ideally regionally controlled tests must be able to be carried out with minimal effort. Low-code technology can achieve enormous time savings here: Sales and product development can be implemented and launched quickly after a short concept and planning phase. If an idea proves viable, it can be pursued further and launched as a product, sub-product, or service.

If the idea turns out to be less promising, the costs incurred are manageable. This allows for multiple tests to be conducted with a comparable effort to previous developments. Furthermore, low-code platforms can be used to test not only individual use cases but also entirely new business models. For example, it’s possible to verify whether the real-time processing of data from a customer or an ecosystem actually works and is correctly priced within the context of the assumptions made by its own actuaries.

External and internal interface capabilities open up new digitalization potential.

Not only are end customers’ demands on insurance companies and their digital service capabilities and quality increasing, especially from Generation Y onwards, but the mutual demands on the digital capabilities of the various market participants in the insurance sector are also growing. The multi-tiered distribution system alone, with its differently connected and operating partners, requires enormous digital interface intelligence.

Digital transformation affects all market participants.

Digital transformation affects all market participants. They face the challenge of deciding whether to modernize their entire IT landscape first—something that has already failed remarkably often, especially in the insurance sector—or to initially focus on new product ideas and improved processes, scaling them later. Low-code helps to consider and test effective approaches to both topics simultaneously. This creates the opportunity to alleviate some of the pressure on the ubiquitous, resource-intensive large-scale projects while simultaneously maintaining a market presence and fostering innovation.

Developer resources in insurance companies are scarce; often, the best specialists get bogged down in day-to-day operations. “Change + Run” initiatives and fresh, innovative approaches are stifled by heterogeneous system landscapes and rigid organizational structures. Low-code platforms can at least mitigate this problem by promoting collaboration between IT and business departments in cross-functional teams. Employees from specialist departments can take on tasks that previously required programming skills, IT staff are relieved of some of their duties and can contribute their expertise where it offers the greatest benefit: A win-win situation for all involved.

Challenges in implementation

Given the significant advantages of low-code, we consider Gartner’s prediction that one in three companies will be using low-code platforms by 2024 to be quite realistic. However, most of these companies still have a lot of work to do before then – especially those in the insurance industry. Why is that? Integrating a low-code application platform into an existing process landscape requires a certain amount of preparation.

The strategies with and without low-code must always be compared. The overall situation results in an evaluation matrix of investments and timelines, which forms the basis for the decision.

As with any use of proprietary software components and services, it is also important with low-code to meet the relevant legal and regulatory requirements (compliance) as well as security requirements. Based on 20 years of experience and a broad customer base among the top 10 insurance companies, SoftProject has extensive experience in evaluating low-code platforms and various usage and licensing models – for example, on-premises, in a private cloud, or in a public cloud.

Involve key users and stakeholders early on

The most important factor for a system’s success is often not the technology’s performance, but rather its acceptance by end users and its ability to respond to constantly changing requirements. Low-code application platforms offer significant added value here, as they enable rapid validation of solutions. Therefore, it is crucial to develop these solutions in collaboration with the actual end users. In projects, companies should systematically plan and retain access to real users and key stakeholders after the initial ideation phase.

Modern low-code application platforms typically offer more than just the ability to develop additional applications. For example, a low-code software platform like the Insurance Gateway can connect existing interfaces and core systems to a data hub, allowing various applications to access data and services. These integration concepts are the company’s internal equivalent of an open data strategy, which can unlock considerable innovation potential within a company.

Low-code platforms are still largely uncharted territory for insurers and brokers. The competitive advantages resulting from its successful implementation are unlikely to remain untapped for long. Given the enormous speed benefits in developing new solutions, this technology could be the booster that propels digital transformation upwards and into a stable orbit. Based on current market feedback, we anticipate that this technology will rise almost as steeply as Apollo 11 did.

Low-Code Platforms: How they make companies successful!

End customers and sales partners expect round-the-clock accessibility via electronic communication channels; insurance companies and their partners must react ever faster to market demands and adhere to short product and time-to-market cycles. At the same time, they are expected to fulfill individual customer requests and provide them with exclusive solutions – all with maximum security and minimal effort. A mammoth task that can be solved with a central low-code digitization platform that connects people, systems, devices, data, and documents, manages data, and automates business processes. But what exactly is a low-code platform, what must it be able to do, and how can insurance companies integrate it into their IT landscape?

First of all: There is currently no universally accepted definition of the term “digitization platform.” Therefore, we will approach it by examining the benefits a company gains from using a digitization platform, such as accelerated workflows, shorter response and processing times, fewer errors, and reduced costs. The ultimate goal is always to increase service and product quality and customer satisfaction. Applications like a chatbot, which allows customers to purchase insurance online – anytime, anywhere, and automatically via an intelligent dialogue system that enables text or voice input, support this process. Other applications allow insurers to communicate with customers on a case-by-case basis. The customer receives a message on their smartphone via SMS or email. A link in the SMS or email takes them to the web application – completely straightforward and without downloading an app. In the event of a claim, messages, images, and invoices can be transmitted electronically. The insurer’s coverage check is also fully automated, and after the claim is assessed, artificial intelligence determines the amount of damage within seconds. Based on predefined rules, the nearest partner garage is identified, and the vehicle is inspected online. The customer then receives a link on their smartphone, allowing them to schedule an appointment independently. A future scenario? No, every advanced digitalization platform must be capable of this.

The first step: Inventory and analysis of the current situation

Before launching any digitization projects, a company must identify processes with potential for improvement. Workshops with digitization experts and a proof of concept have proven effective in this regard.

Following the initial assessment, an evaluation is conducted, outlining concrete proposals for how and where processes can be accelerated, work quality improved, and costs reduced. Subsequently, a process is implemented to demonstrate the interdependencies of the various applications and the functionality of interfaces. This provides the project team with a solid foundation for its further work.

Connectivity: Data must flow freely!

Digitization projects are inherently complex and, if approached incorrectly, can be very costly. Implementation without experts is therefore virtually impossible. The key lies in functioning interfaces between existing IT systems and the digitization components to be integrated. Without the unimpeded import and export of data, process automation is impossible. Special adapters that convert formats and ensure system compatibility guarantee a smooth data flow.

When selecting a digitization platform, it is therefore crucial that it offers industry-specific adapters and connectors. Otherwise, digital patchwork landscapes with isolated information silos and process-inhibiting media breaks can quickly emerge.

Key helpers: Low-code and no-code solutions secure competitive advantages.

Low-code or no-code means that the complexity of the digitalization platform is reduced to such an extent that both business users and process owners can model fully functional, automated processes or system connections on a graphical interface, execute them directly, and monitor and analyze them using dashboards—all without programming. In times of demographic change, where well-trained IT staff capable of implementing complex processes and services are scarce, tools that allow non-developers to graphically implement processes and rules are in higher demand than ever before. These tools enable companies to compensate for limited development resources and scale their operations.

A low-code or no-code platform thus allows companies to reliably meet the increasing demands for agility, flexibility, rapid course correction due to market changes, and even topics such as big data or artificial intelligence. Crucially, the graphical interface of the digitalization platform does not consist solely of drawing tools for process modeling, but rather features digitalization modules with directly executable functions and powerful process engines.

What should a low-code platform be able to do?

Compatible: Easily switch between different platforms and operating modes

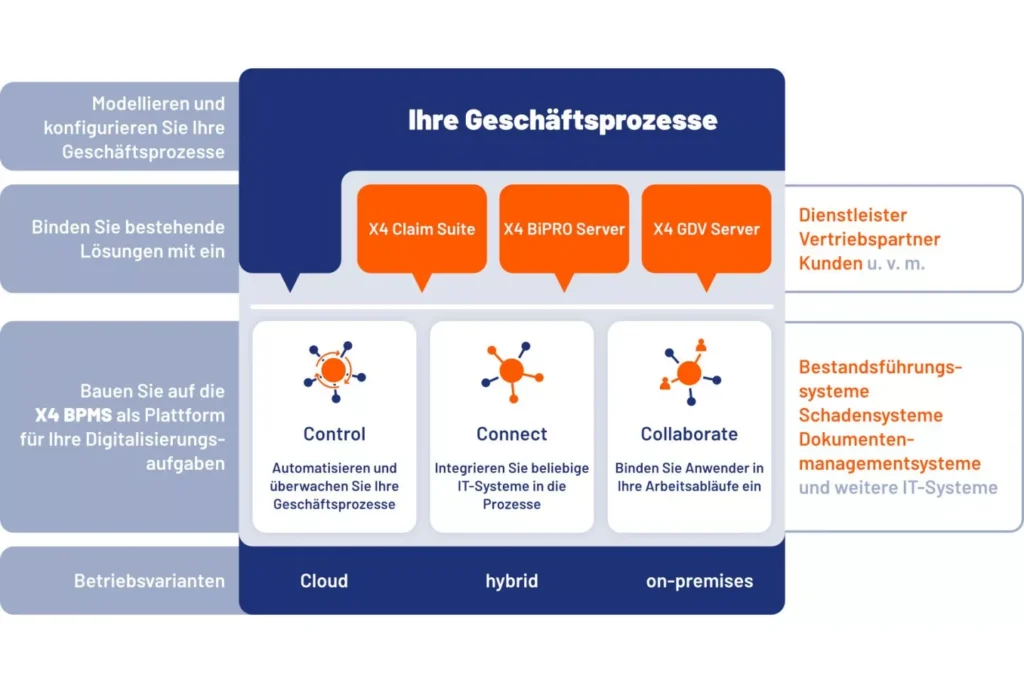

Insurers and their partners can deploy the BPM software X4 BPMS in the cloud, as a hybrid solution, or on-premises. While some companies deploy their applications, services, and data entirely via cloud computing platforms such as Google Cloud Platform, Amazon Web Services (AWS), Red Hat OpenShift Online, or Microsoft Azure—for example, to benefit from flexibility and reduced maintenance costs—others prefer a hybrid approach.

A hybrid operating concept has the advantage that the connection of back-end systems and company-specific processes is operated in the company’s own data center, while typical industry processes, such as connecting any service providers or intermediaries, can be outsourced to the cloud, ideally ISO-certified and operated in Germany—without sacrificing accelerated, agile performance.

Should requirements, strategic direction, or economic considerations change for companies currently relying on a purely on-premises solution, they can upgrade to a hybrid or cloud solution with X4 BPMS at any time. Over 200 adapters make all interfaces compatible.

Perfect interplay: Industry-specific and industry-neutral solutions

The more sub-processes an insurance company automates, the easier further digitalization becomes. This is achieved, for example, by reusing already digitized processes, thus reducing the effort required for further digitalization projects. Numerous forward-thinking companies are already digitizing industry-specific processes and relying on end-to-end electronic claims processing, automated service provider management, portal and self-service solutions for their customers, or the automated implementation of BiPRO and GDV requirements and eNorms.

Pre-built industry solutions, which can also be obtained from the cloud, provide up to 80 percent of the functions to be automated immediately, while only 20 percent require individual customization. Development effort is significantly reduced compared to custom development, costs and expenses are lowered, and services such as web applications and portal solutions are ready for immediate use. Alongside industry-specific solutions, companies are accelerating their digital transformation by automating general, cross-industry business processes such as those in financial accounting or human resources.

¡Abre los ojos! Platform low-code ≠ platform low-code

In summary, every company can and should use a low-code platform to manage current challenges and remain competitive. The designs, definitions, and functions available on the market vary considerably. A thorough review is worthwhile before making a selection. Ultimately, the decisive factor should be that a central platform can handle all digitalization tasks, is field-tested, manages data securely, connects all stakeholders—from insurers and service providers to end customers—and features a low-code or no-code approach, appropriate security tools, and sufficient process depth.